Automatic Savings

Automatic savings methods have become a cornerstone of modern financial planning. With rising concerns about retirement security and emergency savings, people are looking for simple ways to ensure they are setting aside enough money without having to think about it every month. One popular method is payroll deductions, where a set percentage of your income is automatically transferred to a savings account before you even see it.

This method can be incredibly effective in building up savings over time. But like any financial tool, it has its pros and cons. In this article, we’ll explore the effectiveness of automatic savings methods, mainly focusing on payroll deductions, and help you determine whether it’s the right strategy for your financial goals. For those focused on creating a secure financial future, adopting methods like Saving for Future can make a significant difference in achieving long-term stability. Please stay with Aseemoon.

Why People Prefer Automatic Savings Methods

Psychological Benefits

- One key reason people prefer automatic savings methods is the psychological benefit. By automating savings, individuals can remove the temptation to spend money impulsively. This concept, often called “paying yourself first,” ensures that your savings goals are prioritized before other expenses.

Convenience of Payroll Deductions

- Payroll deductions take this convenience a step further by integrating the savings process directly into your paycheck. Once set up, you don’t need to remember to transfer money each month or make manual adjustments. The money is taken out automatically, making sticking to your savings plan nearly effortless.

How Payroll Deductions Work

The Process of Setting Up Payroll Deductions

- Payroll deductions are easy to set up and can usually be done through your employer’s HR department. You decide on a percentage or a fixed dollar amount to be taken out of each paycheck, which is then deposited into a designated account. This could be a retirement account, a savings account, or even an investment account.

Examples of Payroll Savings Plans (401(k), Retirement Savings, etc.)

- Standard payroll savings plans include 401(k)s and IRAs for retirement and health savings accounts (HSAs). These accounts offer additional benefits, such as tax advantages, making saving even more rewarding.

The Benefits of Automatic Savings Methods

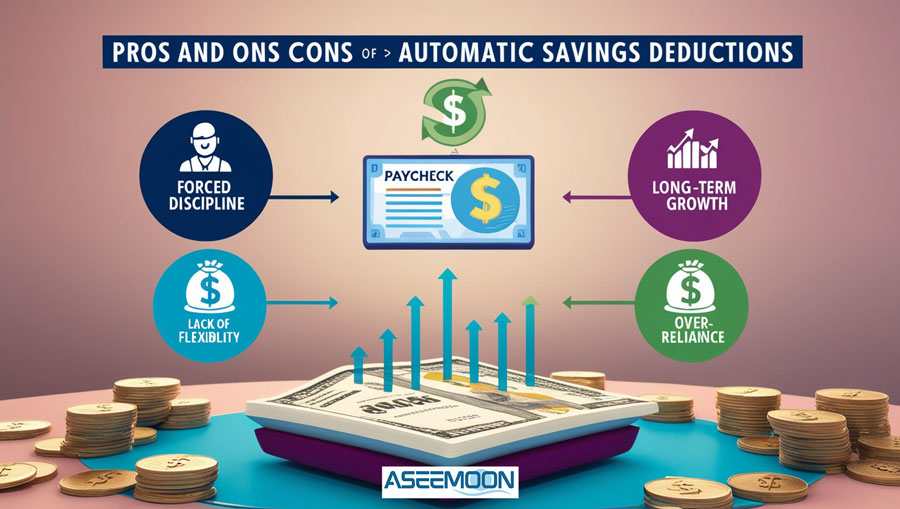

Forced Discipline in Saving

- One of the greatest advantages of automatic savings methods is the forced discipline they create. Because the money is taken out before you see it, spending it’s less tempting. Over time, this discipline can help you build a substantial nest egg.

No Need for Monthly Decisions

- Automatic savings relieve you of deciding how much to save each month. Once your payroll deduction is set up, your savings happen consistently and without any extra effort.

Long-Term Growth and Compound Interest

- You benefit from compound interest by contributing regularly to savings or investment accounts through payroll deductions. Over time, this can lead to significant growth in your savings, especially if you start early.

Potential Drawbacks of Automatic Savings Methods

Lack of Flexibility in Finances

- One drawback of payroll deductions is the potential lack of flexibility. If your financial situation changes unexpectedly, it can be difficult to adjust the amount being deducted without going through your employer’s HR process.

Over-reliance on Payroll Deductions

- Another potential issue is over-reliance on payroll deductions. While they can be an excellent tool for saving, they should be part of a larger, more comprehensive financial plan that also includes manual savings, investments, and emergency funds.

Are Payroll Deductions Right for You?

Assessing Financial Goals and Needs

- Whether payroll deductions are correct for you depends mainly on your financial goals. If you’re looking for a hassle-free way to save for retirement or build an emergency fund, they can be a great option. However, if you prefer more control over your savings or have fluctuating income, manual savings methods might be more suitable.

Choosing the Right Percentage for Payroll Savings

- Deciding on the right amount to save through payroll deductions is key. A good rule of thumb is to start with a small percentage—perhaps 5-10%—and gradually increase it as your income grows or as you become more comfortable with your savings plan.

Common Payroll Deduction Savings Accounts

Payroll deduction savings accounts are essential financial tools that help individuals save for various purposes, including retirement, healthcare, and emergencies. Below is an overview of three common types of payroll deduction savings accounts: Retirement Accounts, Health Savings Accounts (HSA), and Emergency Funds/General Savings.

Here’s a comparison table for the different savings and retirement options you provided:

| Feature | 401(k) Plans | Traditional IRA | Roth IRA | Health Savings Account (HSA) | Emergency Funds | General Savings Accounts |

|---|---|---|---|---|---|---|

| Definition | Employer-sponsored retirement plan | Personal retirement savings plan | Personal retirement savings plan | Medical savings account for HDHP | Savings for unexpected expenses | Savings for various goals |

| Tax Benefits | Pre-tax contributions, tax-deferred growth | Contributions may be tax-deductible, taxed upon withdrawal | Contributions are after-tax, withdrawals are tax-free | Pre-tax contributions, tax-free earnings and withdrawals for medical expenses | No tax benefits | No tax benefits |

| Employer Match | Many employers offer matching | Not applicable | Not applicable | Not applicable | Not applicable | Not applicable |

| Contribution Limits (2024) | $22,500 under 50, $30,000 for 50+ | $6,500 under 50, $7,500 for 50+ | $6,500 under 50, $7,500 for 50+ | $3,850 individual, $7,750 family, +$1,000 if 55+ | No specific limit | No specific limit |

| Withdrawal Rules | Penalties before age 59½ unless exceptions | Penalties before age 59½ unless exceptions | Tax-free withdrawals after 59½ | Tax-free for medical expenses, penalties otherwise | Easily accessible | Easily accessible |

| Key Features | Employer-sponsored tax advantages | Tax-deferred growth, tax deduction | Tax-free growth and withdrawals | Funds rollover annually remains even with job changes | Accessible for emergencies | Accessible for various savings goals |

| Purpose | Retirement | Retirement | Retirement | Medical expenses | Financial security in emergencies | Flexible savings for future spending |

This table highlights the main differences between the various savings and retirement plans, making it easier to compare their features.

Payroll Deductions vs. Other Automatic Savings Methods

When it comes to saving money automatically, payroll deductions and automatic bank transfers are two popular methods. Each has its own advantages and disadvantages, particularly regarding ease of use, risk, and potential returns. Below is a comparison of these two methods.

How Payroll Deduction Compares to Automatic Bank Transfers

Payroll Deductions

- Definition: Payroll deductions involve automatically allocating a portion of an employee’s paycheck to savings accounts, retirement accounts, or loan payments before the funds reach the employee’s checking account.

- Convenience: This method requires a one-time setup through the employer, making it a “set it and forget it” option for savings.

- Tax Advantages: Contributions made through payroll deductions for retirement accounts (like 401(k)s or HS).

- Accessibility: Funds are typically less accessible for immediate spending, which can help prevent impulsive purchases.

Automatic Bank Transfers

- Definition: Automatic bank transfers involve setting up recurring transfers between accounts (e.g., from checking to savings) through the bank’s online banking system.

- Flexibility: Users can adjust transfer amounts and frequencies easily, allowing for more tailored savings plans based on changing financial situations

- Immediate Access: Funds are usually more accessible compared to payroll deductions, which may encourage spending rather than saving.

- No Employer Involvement: This method does not require employer cooperation, making it suitable for self-employed individuals or those without employer-sponsored benefits(+).

Evaluating Risks and Returns

Both payroll deductions and automatic bank transfers serve as effective methods for automating savings. Payroll deductions provide structured savings with potential tax benefits but may limit immediate access to funds. In contrast, automatic bank transfers offer flexibility and more accessible access but require more discipline to ensure consistent savings.

Here’s a comparison table for evaluating risks and returns between payroll deductions and automatic bank transfers:

| Feature | Payroll Deductions | Automatic Bank Transfers |

|---|---|---|

| Risks | – Job loss or change may require reestablishing deductions. – Early withdrawal from retirement accounts may incur penalties. |

– Risk of overdraft fees if the account balance is insufficient. – Inconsistent saving if not properly structured. |

| Returns | – Potential for significant growth through tax advantages and employer matching (e.g., 401(k), IRA). – HSAs offer tax-free growth for qualified medical expenses. |

– Depends on the savings account type. – High-yield savings accounts may offer better interest but generally lower returns than retirement accounts. |

Choosing between these methods depends on individual financial goals, employment status, and personal preferences.

Real-Life Examples of Payroll Deduction Success Stories

Case Study 1: John’s Retirement Savings

Background: John, a 35-year-old software engineer, decided to take advantage of his employer’s 401(k) plan. He set up a payroll deduction of 5% of his gross pay.

- Initial Setup: John’s gross pay is $2,000 bi-weekly. He contributes $100 to his 401(k) each pay period.

- Employer Match: His employer matches 50% of his contributions, adding $50 per pay period.

Results After Five Years: Over five years, assuming an average annual return of 6%, John’s retirement savings grew significantly:

-

- Total contributions: $13,000 (including employer match)

- Account value after five years: approximately $15,000.

John’s disciplined approach to saving through payroll deductions not only helped him build a solid retirement fund but also took advantage of the employer match, maximizing his savings potential.

Case Study 2: Sarah’s Health Savings Account (HSA)

Background: Sarah, a 28-year-old marketing professional, enrolled in her company’s high-deductible health plan and opened an HSA.

- Contribution Strategy: She opted for a payroll deduction of $150 per month into her HSA.

- Tax Benefits: The contributions were pre-tax, reducing her taxable income.

- Usage: For the year, she used the funds for various medical expenses without incurring tax penalties.

- Long-Term Growth: By consistently contributing and allowing her HSA to grow tax-free, Sarah is on track to accumulate significant savings for future healthcare needs.

Sarah’s proactive use of payroll deductions for her HSA not only provided immediate tax benefits but also positioned her for long-term healthcare savings.

Case Study 3: Mark’s Emergency Fund

Background: Mark, a 40-year-old teacher, recognized the importance of having an emergency fund. He decided to automate his savings through payroll deductions.

- Savings Goal: Mark aimed to save $5,000 over the next year.

- Deduction Setup: He arranged for a payroll deduction of $200 each month into a high-yield savings account.

- Outcome: By the end of the year, Mark successfully reached his goal of $2,400 in contributions. With interest accrued from the high-yield account, he ended up with approximately $2,500 saved.

By utilizing payroll deductions for his emergency fund, Mark ensured that he consistently saved without the temptation to spend that money elsewhere.

The automation provided by payroll deductions simplifies the saving process and helps individuals stay committed to their financial objectives.

Common Mistakes to Avoid When Using Payroll Deductions

Utilizing payroll deductions can significantly enhance savings and financial management, but there are common pitfalls that individuals should avoid. Two critical mistakes include:

- Setting inappropriate deduction percentages

- neglecting other financial obligations

Here’s a comparison table summarizing the key points of the common pitfalls when utilizing payroll deductions:

| Issue | Potential Pitfalls | Consequences |

|---|---|---|

| Setting Too High a Percentage | – Reduced take-home pay – Inflexibility in handling unexpected expenses |

– Financial strain, difficulty covering essential bills – Limited ability to handle emergencies |

| Setting Too Low a Percentage | – Insufficient savings growth – Missed opportunities for employer matching |

– Slow retirement growth, inadequate emergency savings – Long-term financial impact |

| Neglecting Other Financial Obligations | – Focusing solely on deductions and ignoring debts or living expenses | – Debt accumulation due to unpaid high-interest debts – Financial instability |

| Impact on Lifestyle and Well-being | – Stress from over-committing to deductions – Ignoring immediate financial needs |

– Anxiety, reduced well-being, missed investment opportunities with higher returns |

To effectively utilize payroll deductions as a savings strategy, individuals should carefully evaluate the percentage they choose for deductions and ensure they do not neglect other financial obligations. Striking a balance between saving for the future and managing current expenses is crucial for achieving long-term financial stability and peace of mind.

Optimizing Your Savings Strategy

Optimizing Your Savings Strategy involves balancing payroll deductions with other savings methods and adjusting your savings as your income changes. Here’s a breakdown of how to achieve both effectively:

1. Balancing Payroll Deductions with Other Savings Methods

- Diversify Your Savings Approach: While payroll deductions are great for long-term savings (like retirement accounts), it’s essential to incorporate other methods for different goals. For example:

- Emergency Fund: Use automatic bank transfers to contribute to a high-yield savings account for short-term needs.

- Investment Accounts: Consider setting up automatic transfers to taxable brokerage accounts for long-term growth.

- Debt Repayment: Allocate a portion of your income toward paying off high-interest debt, which can improve your overall financial health.

- Avoid Overcommitting to Payroll Deductions: Ensure that payroll deductions do not interfere with paying essential living expenses or debts. This ensures you’re not facing cash flow issues due to excessive retirement savings at the expense of your day-to-day financial health.

2. Adjusting Savings as Your Income Changes

- Increase Contributions as Income Grows: As your salary increases, it’s wise to adjust your payroll deductions to align with your new financial capacity. Consider contributing a higher percentage to your retirement accounts or increasing contributions to your emergency fund or investment accounts.

- Review Your Financial Goals Periodically: Every time you experience an income change (a raise, bonus, or even job change), review your savings strategy. You may want to shift more towards aggressive investments or pay off lingering debts faster.

- Avoid Lifestyle Inflation: When your income rises, it can be tempting to spend more. Instead of succumbing to lifestyle inflation, increase your savings to keep your future financial goals in focus.

Conclusion: Weighing the Pros and Cons of Payroll Deductions

In conclusion, automatic savings methods, particularly payroll deductions, can be an effective way to enhance your financial health. They offer convenience, psychological benefits, and the potential for long-term growth. However, they are not without their drawbacks, such as a lack of flexibility and the risk of over-reliance.

Ultimately, the decision to utilize payroll deductions as part of your savings strategy depends on your individual financial goals and preferences. By weighing the pros and cons and incorporating these methods into a broader financial plan, you can work toward achieving your savings objectives more effectively.

FAQs:

What are automatic savings methods?

- Automatic savings methods involve regularly transferring money into savings or investment accounts without manual input.

How do payroll deductions work for savings?

- Payroll deductions automatically divert a portion of your paycheck into a savings account, retirement plan, or investment fund.

What are the pros of payroll deductions?

- Pros include effortless saving, compound interest growth, and building long-term savings.

Are there any downsides to payroll deductions?

- Yes, lack of flexibility and potential over-reliance on automated savings are common concerns.

Can I adjust my payroll deductions?

- Yes, but you usually have to go through your employer’s HR department, which can be a bit cumbersome.

Is it better to use payroll deductions or manual savings?

- It depends on your financial goals and how much control you want over your savings. Both methods have their benefits.